Ask any farmer what the most difficult part of farming is and some percentage of them will say marketing. We can do everything right during the entire year and poor marketing can make it all for naught. Excellent yields can sometimes cover for poor marketing, but it is not the best way to thrive.

Human nature and emotions are some of the hardest things to overcome when it comes to marketing a crop. Both greed and fear can be crippling and prevent us from making decisions.

One thing is almost guaranteed—we will not sell everything at the top of the market. That would require selling the entire crop in one sale and getting lucky enough to pick the one day when the market is at its peak. Doing this is nearly impossible and can mostly be attributed to luck rather than skill or knowledge.

It is best to admit that no matter how good a sale may be, it is likely not going to be the highest price, and that is okay. For this reason, we like to sell in increments and hopefully the weighted average price of all sales is better than two-thirds of the market.

Now that we’ve gone through the philosophical, on to the practical.

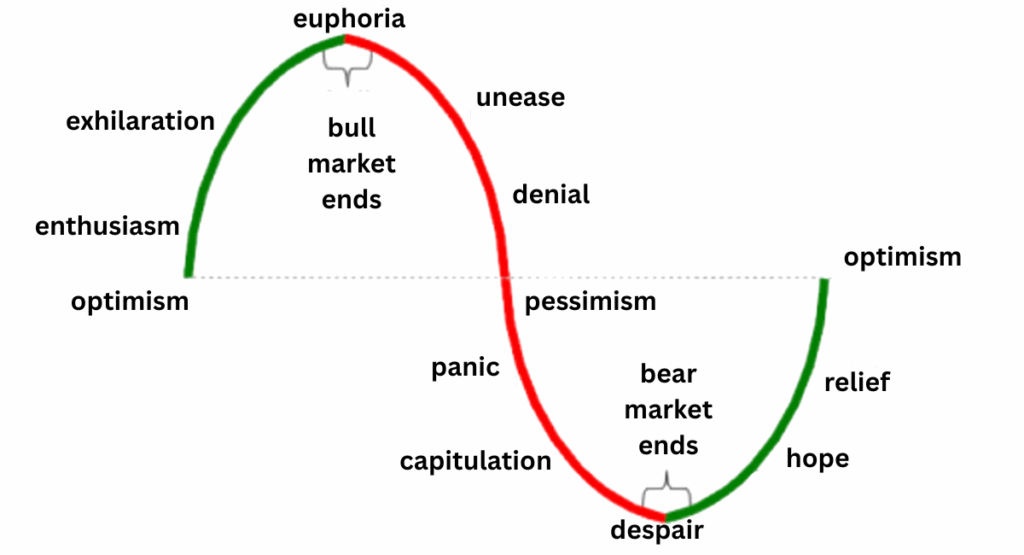

The market cycle graphic below has been used before in this newsletter. The market top and the end of the green line, labeled as “euphoria” was sometime during 2022. We have been riding that red line down since then.

You can decide where we are right now, but that will probably push us back into the human nature and emotions debate.

Market Cycle

Corn

Let’s start with some numbers from USDA. Ending stocks from the 2024 corn crop are currently projected to be 1.365 billion bushels on August 31st. This puts the stocks to use percentage higher, which normally correlates with higher prices than we are seeing currently.

The reason prices are not moving higher is the expected acres we have planted to corn this year. Estimates from government agencies expect farmers to plant over 95 million acres of corn this year. Almost all those expected acres were planted before June 1st, eliminating the chance of a planting delay rally.

Many of the acres left to plant are in eastern states of Ohio and Pennsylvania, not the heart of the corn belt. We could even argue that the relatively dry planting season in the middle and western corn belt allowed more corn acres to be planted than originally intended.

Only two years in the last 50 have we had higher corn acres than this year. In 2012, we planted 97.3 million acres and 2013 saw 95.4 million acres.

The historic drought of 2012 suppressed our national yield to an amazingly low 123.1 bushels per acre. The resulting tight supply and high prices incentivized farmers to plant corn again in 2013, and national yield recovered to 158.1 bushels per acre—slightly below the long-term trendline.

Trendline yield this year is 181 bushels per acre. If realized, this will easily be the largest corn crop we have ever grown in terms of bushels per acre and in total bushels at over 15.8 billion.

Assuming trendline yield and current acreage assumptions, we can expect the 2025 crop ending stocks to be higher on August 31, 2026. Right now, predictions are for an ending stock increase of almost 400 million bushels, up to 1.75 billion bushels. This is 11.3% stocks to use ratio.

USDA’s projected yearly average cash price of $4.20 per bushel would probably fit closely with historical data for that kind of ending stock percentage. Something to keep in mind with this projection; the USDA has lowered the 2024 corn ending stock number during 10 of the last 12 months with a total reduction of 700 million bushels.

If that were to repeat itself, we are close to a 1-billionbushel carryover and much higher prices.

Corn Yield by Year, US

Parts of the southern and eastern corn belt are too wet, while other parts are too dry. There are areas with difficult conditions every year and that is what keeps us from blowing the top off national yield.

2004 could be used as an example of an exceptional growing season where the national yield surpassed expectations by a significant amount. The trendline yield in 2004 was 144.8 bushels per acre and final yield was 160.3 bushels per acre. Although 15.5 bushels per acre doesn’t sound like a lot, it is 10.7% above expectations.

What if we achieved a 10.7% above trend yield this year?

That number would be 200.4 bushels per acre. Many would say a 200 bushel per acre national yield is unrealistic in 2025. While we don’t believe this is likely, historical statistics could argue that it is possible.

Planted corn acreage in 2004 was 80.9 million acres compared to 95 million acres today. It is likely that some of those additional acres are not the best acres for corn production.

Soybeans

Soybeans are in a very different situation than corn. Ending stocks for the 2024 soybean crop are projected to be 350 million bushels on August 31, 2025. This would put the stocks to use percentage at 8.0%. Historically speaking, this is relatively low although we did hang around 6% during the higher price years of 2021-2023.

The difference comes in planted acres. USDA says we will plant about 83.4 million acres of soybeans in the United States this year, down about 3.7 million from last year. Like corn, planting pace ran ahead of average this spring.

The only reason to think we wouldn’t hit that total number of acres planted is because some of the intended soybean acres were switched to corn, or some of the wetter areas in the southern part of the US do not get planted this year.

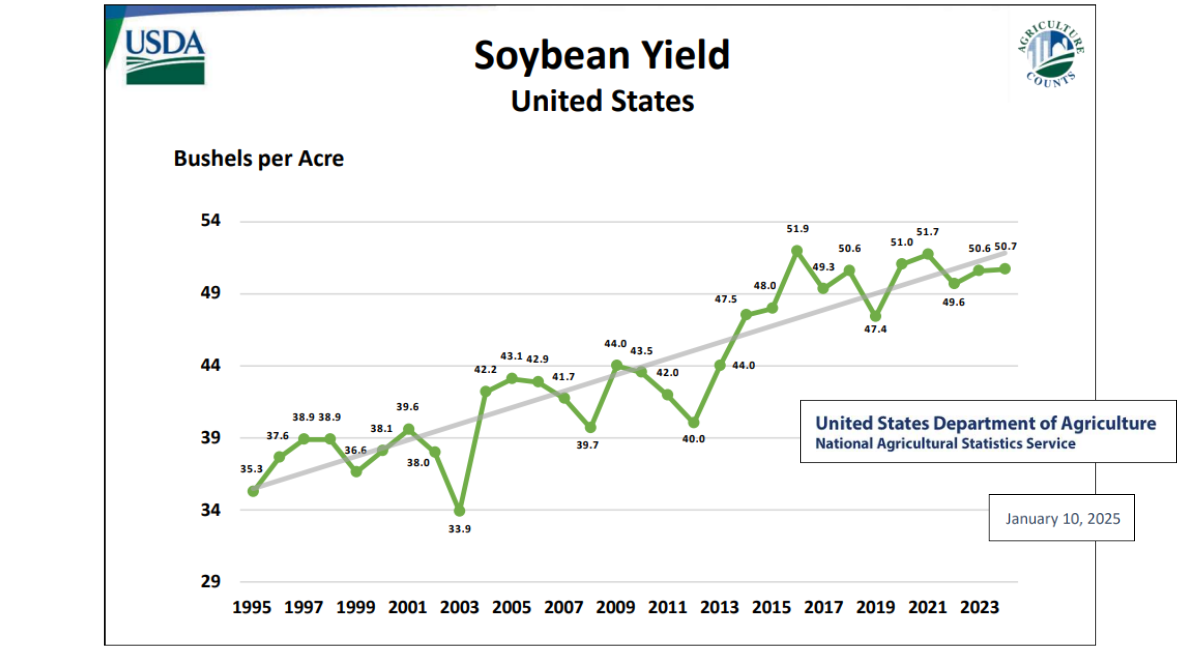

Trendline yield in soybeans is 52.5 bushels per acre this year, which would beat the previous record yield of 51.9 bushels per acre in 2016. Farmers will need to grow an exceptional yield in soybeans this year to even have a chance of not lowering the ending stocks to use percentage.

Current production and usage numbers project a tightening of domestic soybean stocks even if we achieve the new record yield of 52.5 bushels per acre.

Soybean Yield by Year, US

The part that could be interesting is if the soybean yield were to fall short of expectations. Projected ending stocks would fall below 5% domestically, which would likely cause rationing of supply.

The first place to see cutbacks would be in exports. China is the largest consumer of soybeans in the world and our largest soybean buyer. Brazil is the largest producer of soybeans in the world, and they are growing most of their crop with exports in mind. Brazil plans to export 3.9 billion bushels of soybeans this year.

To put that in perspective, the United States is projected to grow 4.3 billion bushels of soybeans this year. The current trade situation with China and the US will likely accelerate the decline in purchases from the United States and be replaced with exports from elsewhere.

Looking at the Other Direction in Soybean Yields

What if we used our 2016 yield compared to projected trendline from that year? Trendline was 45.2 bushels per acre. That puts the actual yield at 14.8% above the trend.

If we were to produce a 2025 soybean yield that was 14.8% above the trend, the final yield would be 60.27 bushels per acre. This seems even more unlikely than the corn scenario mentioned earlier, but this is what the statistics show.

The craziest part of the 60 bushel per acre national yield is that it still would not produce an ending stock surplus as large as the 2018 soybean crop had in August of 2019.

Prices

What does this all mean for prices?

The short answer is, we don’t know. The “summer peak” of the market traditionally occurs in the middle to end of June. That was not the case this year as corn prices are sitting at the lower levels we saw during harvest last fall.

As of today, the highest prices we have seen since the beginning of the marketing year were in February. If that were to hold, it would only be the second time since 1970 this has happened in corn.

Soybeans are also significantly lower than last year. July is the month most likely to see the highest prices offered for soybeans according to historical data. We still have time for a weather rally, but it will have to be a late summer drought or extreme heat during grain fill rather than a full season lack of moisture.

Agriculture Cycles

One thing we can usually count on is that history repeats itself. Cycles in agriculture are nothing new and all we can really do in most years is try our best to learn from the past and apply it to the future.

As mentioned at the beginning, removing emotions and looking at data can help us make better decisions going forward.

Partner with Stalcup

For more than 75 years, Stalcup has partnered with landowners to help them make the most of their farmland. Rooted in northwest Iowa, our team brings deep knowledge of the local ag economy, tenant relationships, and land stewardship priorities that matter to owners.

Whether you’ve had the same tenant for decades or are just beginning to explore your options, we’re here to serve as your boots on the ground—ensuring your land remains both productive and well cared for.

Even if you prefer to manage your farm independently, a farm manager can provide objective support with things like reviewing lease agreements, assessing crop performance, or navigating tenant changes.

Curious if farm management is a fit for you? A one-on-one consultation can help clarify your options and align services with your long-term goals.

Read more from Today’s Land Owner Summer 2025: